Interest rates remain one of the most important economic factors impacting commercial real estate values, transaction activity, development feasibility, and investor sentiment. After one of the most aggressive tightening cycles in modern history, markets are now asking a different question:

Where do rates go from here?

Over the past three years, the Federal Reserve has moved interest rates from near-zero pandemic-era levels to significantly higher levels intended to combat inflation. While inflation has moderated from peak levels, the Federal Reserve continues to balance competing pressures involving inflation, employment, economic growth, consumer spending, and geopolitical uncertainty.

A major point of discussion in financial markets today is the transition in Federal Reserve leadership and whether a new chair could materially influence the future direction of interest rates.

The Role of the Fed Chair — and the Limits of That Role

Recently, Kevin Warsh has received significant national attention following his appointment as Chair of the Federal Reserve. Warsh previously served as a Federal Reserve Governor from 2006 to 2011

and was heavily involved during the 2008 financial crisis. Prior to the Federal Reserve, he worked at Morgan Stanley and served in economic advisory roles during the George W. Bush administration.

Warsh has generally been viewed as more skeptical of expansive monetary policy and has publicly criticized aspects of the Federal Reserve’s post-pandemic actions, particularly related to inflation and balance sheet expansion.

However, it is important to recognize that the Federal Reserve Chair is only one vote within the Federal Open Market Committee (FOMC). While the Chair has significant influence over communication, agenda-setting, and market expectations, monetary policy decisions are ultimately determined by committee vote, not unilateral authority. Even a new Chair with strong opinions on inflation or economic growth must still navigate broader committee consensus and incoming economic data.

In other words, changing the Chair does not automatically mean a dramatic or immediate change in interest rate policy.

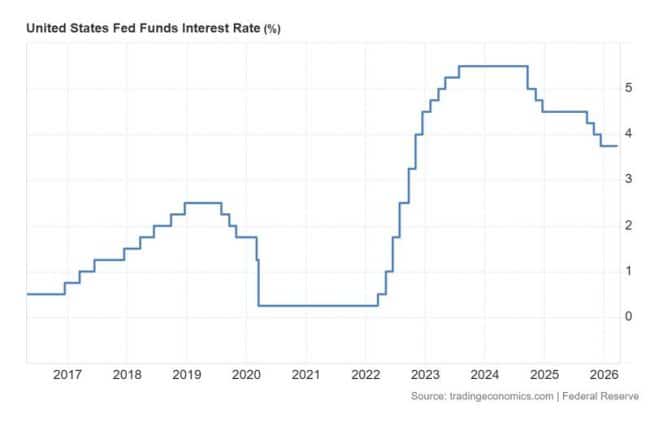

Federal Funds Rate Trend — Last Three Years

The chart below summarizes the general movement in the Federal Funds Rate over the last three years on a quarterly basis, reflecting the Federal Reserve’s aggressive response to inflation followed by a more cautious stabilization period. Data sourced from the Federal Reserve Bank of St. Louis (FRED).

What Could Happen Next?

Several competing forces will likely influence future interest rate policy:

- Persistent inflation pressures

- Labor market strength or weakness

- Energy prices and geopolitical events

- Federal deficit spending and Treasury issuance

- Consumer confidence and spending patterns

- Commercial real estate market stress

- Banking system liquidity and credit availability

Some market participants expect gradual rate reductions over time if inflation continues to cool. Others believe rates may remain elevated longer than many anticipated due to structural inflation concerns and federal fiscal pressures.

For commercial real estate, the ultimate impact extends beyond the Federal Funds Rate itself. Treasury yields, credit spreads, lender appetite, capitalization rates, and investor confidence often matter just as much — and sometimes more — than the Fed’s benchmark rate alone.

As markets continue to evaluate the direction of monetary policy under new leadership, one question remains central for investors, lenders, developers, and property owners alike: Where will rates go next?